When Starting Points Matter

What Valuations and Yields Can Tell Us About Future Relative Returns

On Tuesday I released a book recommendation post in which I poked fun at forecasting. While this article is not a forecast, it’s worth keeping that context in mind as you read.

In two earlier posts, I explored well-documented historical patterns:

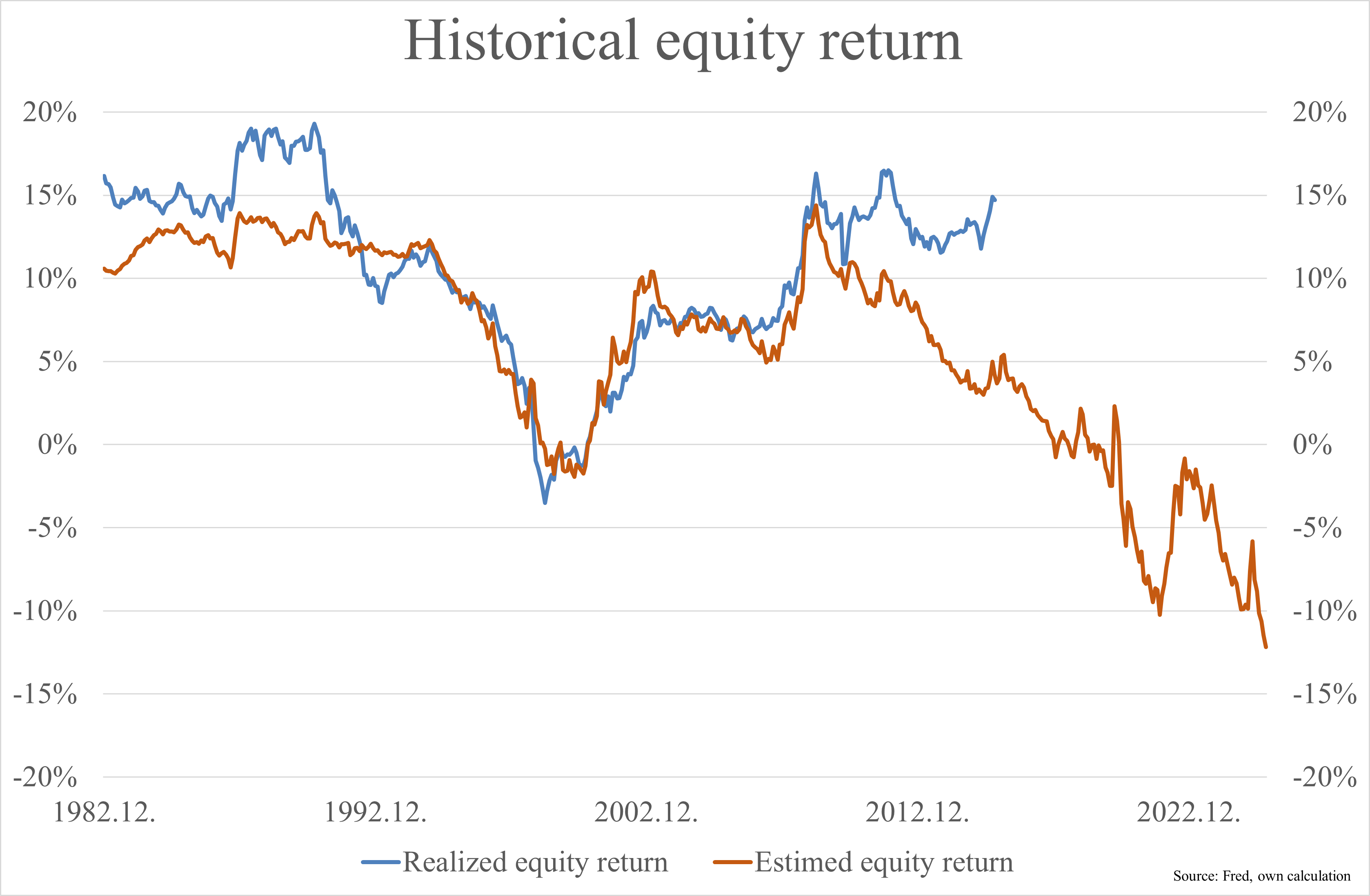

The link between starting equity valuations and long-term stock returns (here)

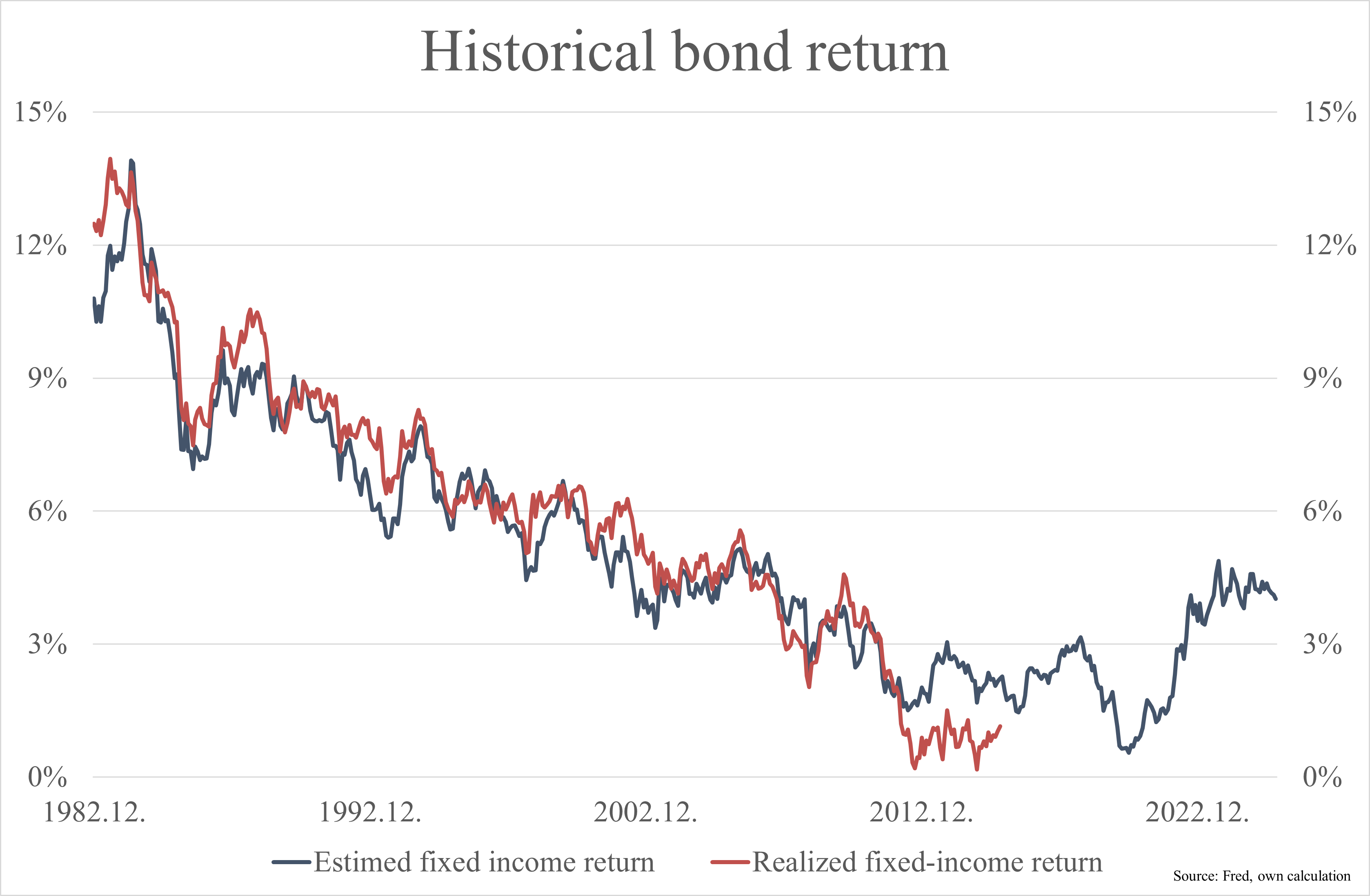

The connection between bond yields (yield to maturity) and subsequent bond returns (here)

If you haven’t read those, start there for important context.

In this piece, I bring together insights from both equity valuations and bond yields to address a central thesis: historical starting conditions - specifically valuations and yields - have shaped, though not determined, the long-term relative performance between stocks and bonds.

Not to predict the future - no model can do that - but to understand what history tells us about market behavior when valuations or yields begin from certain levels.

With this foundation in place, why examine these two ideas together?

Most investment commentary focuses on the absolute performance of a single asset class: “How much will stocks return?” or “What can we expect from bonds?”

Investment choices rarely happen in isolation. Allocators, funds, portfolios, and individuals navigate trade-offs among risk, return, and the opportunity cost of one asset relative to another.

Whether consciously or not, everyone makes relative decisions.

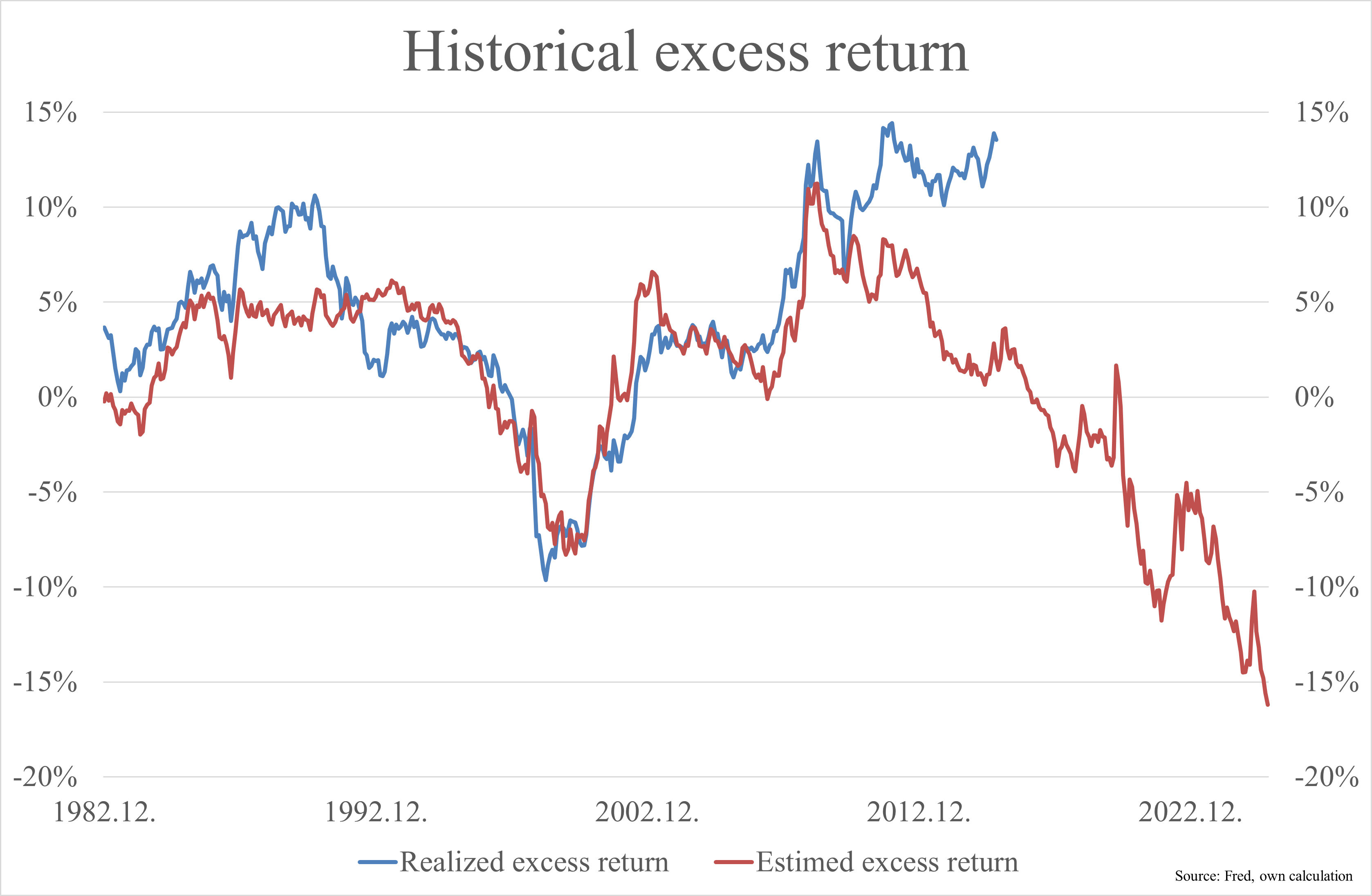

If starting valuations inform long-term equity returns, and yields inform bond returns, then the expected return gap is a meaningful concept.

This “gap” is not a forecast. It’s an observation of historical tendencies: certain starting points are associated with certain outcomes.

The Historical Logic Behind Expected Return Gaps

Let me summarize the intuition without re-explaining the models from earlier posts.

For stocks:

When valuations have been high, subsequent 10-15-year returns have historically been lower.

When valuations are low, later returns tend to be higher.

For bonds:

When yields have been high, bonds have historically delivered higher future returns.

When yields have been low, they have tended to deliver lower future returns.

Combine these observations, and you get something straightforward but informative: The relative positioning of stocks versus bonds is not constant - it shifts over time, depending on starting valuations and starting yields.

Sometimes stocks are priced in ways historically associated with relatively higher future returns. Sometimes bonds have been. Most of the time, the difference hasn’t been dramatic.

But occasionally, the gap has widened or narrowed significantly.

Appreciating this expected return gap clarifies why market environments and investment challenges shift over the decades - building on the main thesis that starting points provide critical historical context.

Why Relative Expectations Matter More Than Precise Forecasts

A common misconception in investing is that one must forecast precise future returns to make rational decisions.

That’s not necessarily true.

Understanding relative opportunity, influenced by starting conditions, is often more valuable.

To illustrate, consider two historical scenarios:

1. When valuations have been high and yields low

Historically, this environment has often been associated with:

Compressed equity risk premiums

Future returns for stocks that weren’t dramatically higher than bond returns

Greater sensitivity to macroeconomic shocks

This doesn’t mean “sell stocks.” It simply describes historical patterns in which the compensation for bearing risk may have been lower than usual.

2. When valuations have been low and yields high

Historically, this combination has often offered:

Attractive long-term equity returns

Attractive long-term bond returns

A wider expected return gap favors equities

Again, this observes history, not a recommendation.

The essential takeaway: the expected return gap has shifted with the starting environment, shaping investment regimes over time.

At this point, you might wonder: Is this just market timing? This distinction is important.

“Market timing” typically implies making short-term directional bets based on near-term price movements.

What we’re discussing here is different:

It’s long-term focused.

It’s structural in nature.

It’s valuation-driven

It unfolds over decades, not weeks or months.

Understanding long-term expected return patterns is not about predicting next year’s prices. It’s about recognizing the investment environment you’re operating within.

Markets have historically been cyclical. Risk premiums have expanded and contracted. Starting conditions have mattered.

None of this constitutes market timing in the traditional sense. It’s context.

Why This Matters for Investors and Asset Allocators

Institutions, managers, and investors weigh risk, cost, compensation, and alternatives.

Relative return expectations influence everything from pension fund liability matching to household savings behavior. Even if you don’t explicitly calculate expected risk premiums, your portfolio decisions already reflect them implicitly.

Recognizing these structural forces helps put market debates into perspective, especially during periods of very high or very low valuations.

The Real Goal: Better Context, Not Crystal Balls

The central thesis is this: while initial valuations and yields do not dictate future returns with certainty, they do shape long-term relative expectations between asset classes.

Understanding the historical connection between starting valuations, starting yields, and subsequent outcomes can help us become more informed investors - not prophets or forecasters, but students of market history.

The patterns we observe in data reflect tendencies, not guarantees. Market environments change. Structural shifts occur. New factors emerge.

What remains valuable is the discipline of thoughtfully examining starting conditions, understanding historical context, and recognizing that different market environments have historically offered distinct opportunity sets.

If you enjoyed this, explore more articles and ideas on my blog here.

Disclaimer

The views and opinions expressed on this website are for educational and informational purposes only, and should not be considered as investment advice. The author may hold positions in the stocks mentioned on this website. The author of this website is not a licensed stockbroker or financial advisor. Nothing contained herein should be construed as a recommendation to buy, hold, or sell any securities or financial products. Always seek the advice of a financial advisor and do your own independent research before making any trade or investment decisions.

We do not guarantee the accuracy or completeness of any information on this website. Such information is provided “as is” without warranty or condition of any kind, either express or implied. Past performance may not be indicative of future results. This website could include inaccuracies or typographical errors.

We are not liable or responsible for any damages incurred whatsoever from actions taken from information provided on this website, including financial losses. Since all readers who access any information on this website are doing so voluntarily and of their own accord, any outcome of such access is understood to be their sole responsibility. In no event shall we be liable to any person for any decision made or action taken in reliance upon the information provided herein.