In your smartphone, your solar panel, and the vault of monetary history, silver is everywhere, and almost nowhere in the conversation. It is time to look at it properly.

There is a metal threading through the whole of modern civilisation that almost nobody talks about. It sits inside the device you are reading this on, in the conductive paste printed onto solar panels going up on rooftops from Bavaria to Bangalore, in the X-ray machines of every hospital, in the wiring of 5G towers, in the contacts of every electrical switch your home contains. A few centuries ago, it funded the Spanish Empire, triggered the first recorded global inflation, and gave the English language the word ‘dollar.’ It is silver - and it has been operating in gold’s shadow for so long that most serious investors have stopped looking at it carefully.

Silver is the only element on the periodic table that has served simultaneously as civilisation’s money and civilisation’s industrial engine. That dual identity is what makes it analytically interesting in a way that gold is not. Gold sits in vaults and waits. Silver works for a living - and increasingly, the world cannot function without it.

This article is an introduction to that story: where silver came from in the monetary order, what has happened to it industrially, why its supply structure is stranger than most people realise, and what the market data currently shows.

Money Before Paper: Silver’s Long Monetary Heritage

Long before gold became the dominant monetary metal of the modern age, silver was the workhorse of commerce. The Roman denarius - the coin that paid legions and priced grain across three continents - was a silver coin. For most of recorded history, ordinary economic life happened in silver. Gold was for sovereigns and central reserves. Silver was for markets.

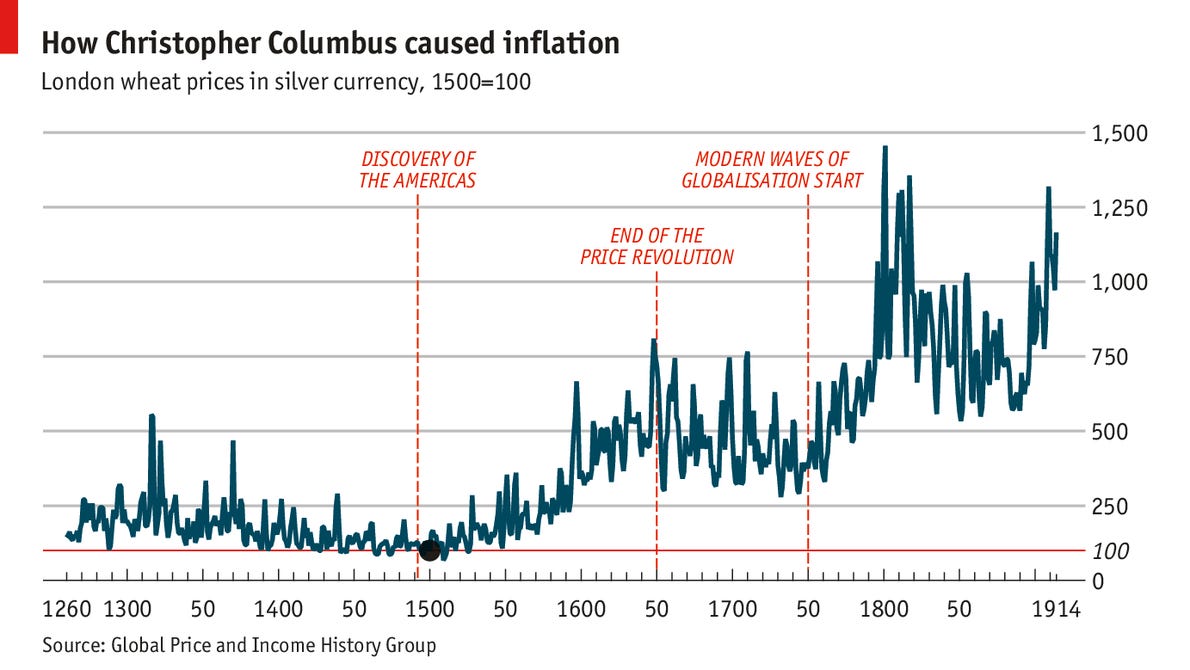

The most illuminating episode in silver’s monetary career - and one of the cleanest natural experiments in the history of monetary theory - is what happened after the Spanish conquest of the Americas. When the Potosí mines of what is now Bolivia were opened in the 1540s, the Spanish found themselves sitting atop the largest silver deposit the world had ever encountered - a mountain, quite literally, of silver ore. Over the following century, an extraordinary torrent of metal flooded into the European monetary system via Seville. Historical estimates of total output vary considerably, but scholars broadly agree that the Potosí mines disgorged tens of thousands of tonnes of silver over their most productive period - enough, by most accounts, to double the European money supply within a generation effectively.

The consequence was what historians call the Price Revolution: a sustained, multi-decade rise in prices across Europe that contemporaries found deeply disorienting and that economists have been analysing ever since. The Flemish economist Jean Bodin identified the mechanism at the time. The scholastics of the Salamanca School - the Spanish precursors of what we later called sound money theory - analysed it in real time with remarkable precision. The money supply expanded massively, not through the decree of any sovereign or the policy of any central bank, but through the brute geological accident of finding a mountain made of silver. The consequence was exactly what sound money theory predicts: the purchasing power of the monetary unit fell, systematically and over a sustained period, in proportion to the increase in supply. It is monetary debasement through abundance rather than through coin-clipping, and it teaches the same lesson.

The word ‘dollar’ is itself a silver inheritance. It derives from ‘Thaler’ - an abbreviation of Joachimsthaler, a coin minted from a Bohemian silver mine from 1518 onward. The Thaler became so widely circulated and trusted that its name became the generic term for a large silver coin across much of Europe and eventually the Americas. When the United States defined its currency unit in the Coinage Act of 1792, it specified a fixed weight of silver. The dollar was originally a silver coin.

Silver’s demotion from monetary metal to commodity was gradual in theory and abrupt in practice. The great bimetallic debates of the 19th century - gold versus silver as the monetary standard - were among the most politically charged economic arguments of the era, but gold ultimately prevailed. Silver was progressively demonetised through the 20th century, with the last major monetary link, the US Treasury’s silver certificates, severed in the 1960s. By then, however, something entirely new had begun happening to silver that no monetary economist had anticipated.

From Vault to Factory: The Industrial Revolution of Silver

As silver was being expelled from the monetary system, industry was discovering just how extraordinary its physical properties are. Silver has the highest electrical conductivity of any element. It has the highest thermal conductivity. It has remarkable antimicrobial properties that hospitals have exploited for over a century. And, critically for the 21st century, it is essential to photovoltaic solar cells: the silver paste screen-printed onto panels conducts the electricity they generate. At present, no substitute has achieved commercial-scale deployment in mainstream cell architectures. However, copper-based metallization is advancing rapidly and beginning commercial deployment in certain cell types - a development that could alter the demand picture meaningfully over the next decade.

The industrial demand story has layers. Photography consumed enormous quantities of silver throughout the 20th century - at its peak in the 1990s, photographic applications accounted for roughly a third of total global silver demand. The digital revolution destroyed that category at an unusual speed. Between 1999 and 2015, demand for photographic silver fell by approximately 90 per cent, and for a period, many analysts concluded that silver had lost its industrial future. This was a reasonable inference from incomplete data. What the photographic collapse actually demonstrated was not that silver demand was fragile, but that silver demand was mobile - capable of migrating from one application to another as technology evolved. Electronics absorbed much of the slack as photography declined. Solar has since dwarfed both. The lesson is not that any single demand category is permanent. Still, that silver’s combination of physical properties - conductivity, reflectivity, antimicrobial action - ensures it finds new industrial homes as old ones close. Photography’s collapse was not the end of the story of silver demand. It was a chapter break.

Every smartphone contains silver. Every laptop, server, and data centre switch. The contacts in electrical relays, the solder in circuit boards, the conductive layers in touchscreens - silver is embedded, invisibly, in almost every device the modern economy runs on.

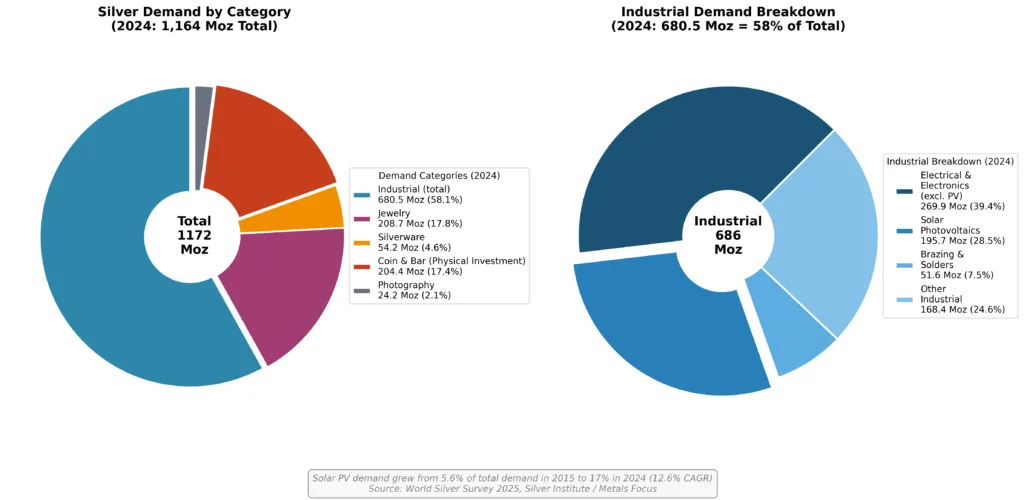

But the demand category that has changed the calculus most dramatically is solar energy. In 2024, the photovoltaic industry consumed approximately 6,600 tonnes of silver - representing around 19 per cent of total global silver demand, up from just 5 per cent a decade earlier. To make that concrete: each gigawatt of solar panel capacity requires roughly 700,000 troy ounces of silver. The world installed over 600 gigawatts of solar in 2024 alone. The International Energy Agency projects that more than 4,000 gigawatts of new solar capacity will be added by 2030. Run the arithmetic, and the scale of what is coming becomes difficult to dismiss.

Crucially, silver in solar panels is in a different category from most other industrial uses. Electronics recycling - circuit boards, industrial scrap, end-of-life devices - does recover meaningful quantities of silver and is an established part of the supply chain. Solar panels are different. Silver screen-printed onto photovoltaic cells is technically recoverable. Still, it is currently rarely recovered: recycling infrastructure for end-of-life panels barely exists, the economics are poor, and panels installed today will not reach end-of-life for 25 to 30 years. As solar deployment accelerates, this represents a structural, growing, permanent withdrawal from available stocks, with no meaningful recycling offset on any near-term timescale. Meanwhile, the shift toward higher-efficiency N-type solar cell technology is actually increasing silver intensity per panel rather than reducing it - newer designs require silver on both the front and rear of the cell, increasing loading by roughly 50 to 100 per cent compared to the previous generation, depending on cell architecture.

Add electrification beyond solar - electric vehicles use up to 50 grams of silver per car, roughly twice that of a conventional combustion engine vehicle; 5G infrastructure is silver-intensive; AI data centres are multiplying globally and require significantly more silver per server than conventional data centre equipment. Beyond electrification, silver’s antimicrobial properties drive demand in medical devices, wound dressings, and water purification systems - applications that are growing steadily, if less dramatically, than solar. Antibacterial textiles represent a smaller but real category. None of these individually rivals photovoltaics in scale, but collectively they reinforce the picture of demand growing across multiple independent vectors simultaneously. Silver has become a strategic industrial input, and the world is only beginning to reckon with what that means for the market.

A Peculiar Mine: Why Silver Supply Cannot Simply Follow Demand

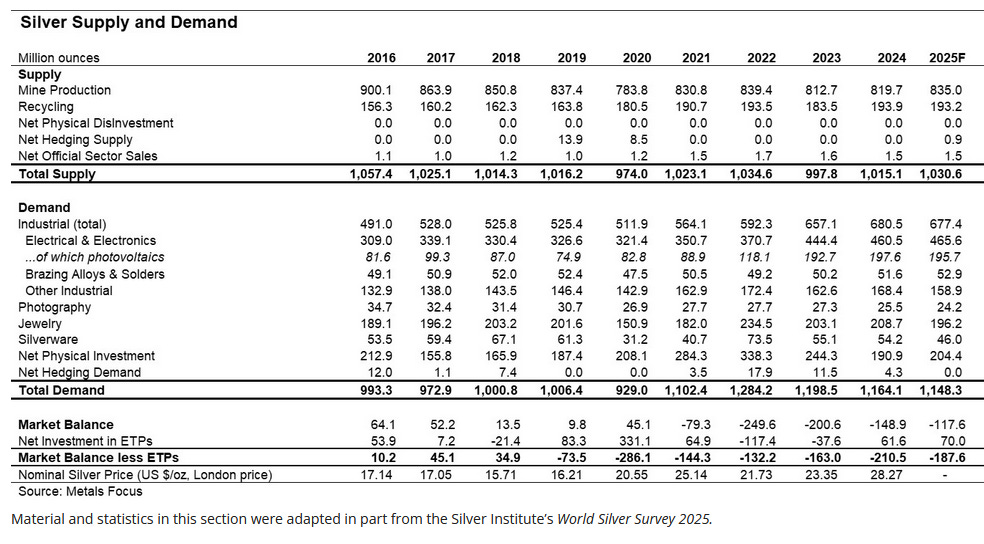

Here is something that surprises most people when they first encounter it: the majority of the world’s silver is not mined by silver miners. Approximately 70 to 75 per cent of annual silver production comes as a byproduct of operations targeting other metals - primarily copper, gold, lead, and zinc. The silver is recovered from ore that was being processed for something else entirely. The miners are not there for the silver.

This creates a supply dynamic unlike that of almost any other major commodity. All mined metals indeed share long lead times - new mines typically require five to ten years of prospecting, permitting, and construction before producing an ounce. But silver faces an additional constraint that most metals do not. When copper becomes expensive, copper miners expand capacity - and as a direct consequence, more silver enters the market as a byproduct, whether the silver price justifies it or not. The reverse is equally true: rising silver prices do little to accelerate production decisions by the copper, zinc, lead, and gold miners who control nearly three-quarters of global silver output. They are not there for the silver, and no price signal directed at silver will change that.

The practical consequence is that silver supply cannot respond quickly to demand shocks the way most commodity supplies can. The primary silver mines - a relatively small group - can and do respond to price signals, but they account for only a minority of production. New primary mine development takes 5 to 8 years from discovery to production. The byproduct base cannot be redirected. This is a structural constraint baked into the geology of silver’s occurrence in the Earth’s crust, which means the market’s ability to balance itself through supply expansion alone is severely limited.

A specific geographical concentration makes this constraint more acute than it might appear on aggregate. Mexico is the world’s largest silver-producing country, accounting for roughly 28 per cent of global mine-site silver output and an estimated half of all primary silver mine production. That single jurisdiction therefore carries outsized weight in any realistic assessment of future supply. Two overlapping problems have emerged there simultaneously. The first is a depleted project pipeline: between 2022 and 2024, the Mexican government effectively froze the permitting process for new mining projects, leaving the sector with a dearth of advanced-stage developments today - precisely when the global market most needs new primary supply. The second is a deteriorating security environment. Cartel violence, which has long been a background feature of operating in Mexico, has moved sharply to the foreground. The January 2026 kidnapping and killing of workers at a silver mine in Sinaloa was a signal that mine personnel had become direct targets. The subsequent killing of the CJNG cartel leader El Mencho in February 2026 - far from stabilising the situation - triggered retaliatory violence across more than twenty Mexican states, as cartel fragmentation typically produces a surge in localised extortion and kidnapping rather than a reduction in overall instability. The states of Zacatecas and Chihuahua, which together account for roughly 45 per cent of Mexico’s total mining output, have not yet seen the worst of the violence - but they represent precisely the territory that competing factions have the strongest economic incentive to contest. New project development in this environment is not merely slow. For many operators and investors, it has ceased to be a viable near-term option.

Five Years of Deficit — and Counting

The Silver Institute has now reported five consecutive years of supply deficit - meaning total demand has exceeded combined mine production and recycling every year since 2021. Over the first four of those years, the cumulative shortfall reached approximately 678 million troy ounces, equivalent to roughly ten months of global mine production drawn down from above-ground stockpiles. The 2024 deficit alone was estimated at around 149 million ounces. A peer-reviewed study published in 2025 projects that by 2030, annual supply may meet only 62 to 70 per cent of demand - a structural gap, not a cyclical one.

This is not yet a crisis. Above-ground inventories exist, and the market clears through their drawdown. But the direction of travel is unambiguous. Industrial demand is growing structurally, driven by the energy transition and electrification. The byproduct dynamic constrains mine supply. Recycling cannot compensate for the gap, particularly when a growing share of silver use - solar panels - produces almost no recyclable material on any near-term timescale.

There is also the investment demand dimension, which adds a layer of volatility that pure industrial metals do not carry. Silver occupies an unusual position: it attracts monetary and investment demand from those who view it as a store of value, layered directly atop its industrial base. When monetary anxiety rises - when confidence in paper currencies or the financial system wobbles - investment demand for silver can spike sharply and rapidly. This happened when silver approached $50 per ounce in 2011, and it has happened in smaller episodes since. The industrial floor is rising. The monetary ceiling is, in principle, open.

A geopolitical dimension has now been added to this picture that was absent as recently as 2024. China - the world’s second-largest silver producer and, more significantly, the dominant force in refined silver, accounting for an estimated 60 to 70 per cent of globally traded refined metal - introduced a licensing regime for silver exports effective January 1, 2026. Under the new rules, only 44 state-approved companies are permitted to export silver, replacing a quota system that had been in place since 2000. Chinese state media described the move as formally elevating silver from an ordinary commodity to a strategic material, placing it under the same regulatory framework as rare earths, tungsten, and antimony. Separately, the United States added silver to its national critical minerals list in late 2025, citing its role in electrical circuits, batteries, solar cells, and defence applications. The significance of China’s position cannot be overstated: even though Mexico produces more silver by mine output, China processes and refines a disproportionate share of global supply. Tighter Chinese export controls do not merely reduce one country’s contribution - they introduce a chokepoint into the global supply chain at precisely the point where the structural deficit is already most acute.

What emerges is a market with growing structural demand, inelastic and largely unresponsive supply, five consecutive years of deficit, a geopolitical supply constraint of recent and potentially growing significance, and a dual identity - industrial necessity plus monetary alternative - that conventional commodity analysis is poorly equipped to model. This is not a price prediction. Markets can remain in deficit for extended periods before prices fully adjust, and other factors intervene. But the structural picture is worth understanding clearly and honestly, and it is a picture the mainstream financial press rarely draws with any precision.

The counterarguments deserve honest engagement. The most serious is substitution, but it is better understood as a question of timing rather than of direction. Copper-based metallization in solar cells is advancing, and early commercial deployments by manufacturers including LONGi and AIKO Solar suggest the technology is maturing faster than most projected even two years ago. If copper achieves broad adoption across mainstream cell architectures, the photovoltaic demand growth story changes materially. Thrifting - the ongoing reduction of silver content per cell - has already compressed silver intensity faster than many forecasts anticipated. Above-ground stockpiles, while being drawn down, have not yet reached critically low levels, which means the market can absorb deficits for some time before a disorderly adjustment becomes likely. A structural imbalance does not resolve on a fixed timetable. The appropriate conclusion is not that the bull case is certain, but that the variables most likely to resolve it - substitution at scale, accelerated recycling, new primary mine supply - each face their own multi-year lead times. The imbalance may be corrected. It is unlikely to be corrected quickly.

The Restless Metal

Roy Jastram, the economic historian who wrote the definitive long-run study of silver’s purchasing power, called it the ‘restless metal’ - a name earned through centuries of price volatility that stood in sharp contrast to gold’s relative stability. Jastram was writing in 1981, before photovoltaics, before the electronics revolution, before the energy transition became the defining infrastructure project of our era. His label still fits, but the source of the restlessness has changed fundamentally.

Silver began as money and became an industry. It was demonetised, rediscovered, hammered by the collapse of photographic demand, rescued by electronics, and is now being pulled hard - structurally, durably - by the solar revolution and the broader electrification of the global economy. At every turn, it has been underestimated, partly because it exists in gold’s shadow and partly because its dual nature makes it genuinely difficult to categorise and therefore easy to dismiss.

That dismissal, the data suggests, may be becoming more expensive to sustain.

What This May Mean for Investors

Markets rarely reward structural understanding immediately. Imbalances between demand and supply can persist for years, and valuation adjustments seldom unfold on a timetable that aligns with investor expectations. Silver’s unusual position - as both an industrial necessity and an intermittently sought monetary alternative - has historically made it particularly prone to long periods of neglect followed by sudden phases of intense attention. Assets with such characteristics tend to test conviction before they reward it.

For investors who already regard gold as a form of monetary insurance, silver introduces a different behavioural challenge. It does not offer the same stability of narrative or price action. Instead, it moves in response to a shifting mix of technological demand, monetary sentiment and speculative positioning. This complexity can make it harder to hold through extended periods when its relevance appears diminished, even as underlying fundamentals continue to evolve.

In a portfolio context, the most useful question may not be where silver is likely to trade next, but what role it might play across different economic environments. Assets that combine structural industrial demand with constrained supply dynamics often introduce both opportunity and discomfort. They can enhance long-term purchasing power during certain phases while imposing volatility that tests an investor’s tolerance for uncertainty.

History offers perspective rather than certainty. Investors who approach silver primarily through the lens of short-term performance may find it persistently frustrating. Those who view it as part of a broader effort to navigate monetary change, technological transition and valuation cycles may instead recognise it as a source of optionality - an asset whose significance becomes clearer across regimes rather than within a single market narrative.

Silver has more than doubled in 2025 — does that represent the market finally catching up with the fundamentals, or just the beginning of a much larger repricing?

Thanks for reading! Let me know your thoughts in the comments. — Attila

If you enjoyed this, explore more articles and ideas on my blog here.

Disclaimer

The views and opinions expressed on this website are for educational and informational purposes only, and should not be considered as investment advice. The author may hold positions in the stocks mentioned on this website. The author of this website is not a licensed stockbroker or financial advisor. Nothing contained herein should be construed as a recommendation to buy, hold, or sell any securities or financial products. Always seek the advice of a financial advisor and do your own independent research before making any trade or investment decisions.

We do not guarantee the accuracy or completeness of any information on this website. Such information is provided “as is” without warranty or condition of any kind, either express or implied. Past performance may not be indicative of future results. This website could include inaccuracies or typographical errors.

We are not liable or responsible for any damages incurred whatsoever from actions taken from information provided on this website, including financial losses. Since all readers who access any information on this website are doing so voluntarily and of their own accord, any outcome of such access is understood to be their sole responsibility. In no event shall we be liable to any person for any decision made or action taken in reliance upon the information provided herein.

Demand remains a big question if worldwide recession due to energy and fertilizer situation in Persian Gulf. Do we know that solar manufacturing remains on high levels or is this market becoming somewhat saturated and liquidity allowing to finance solar drying up?

It is up to us to remember that silver is money. Silver could be a Tier Zero asset. I Hand you a coin, ZERO outsiders would know about our transaction. Old folks here now and then use the word ‘Silber’ I/ of Geld. Holding a heavy solid silver coin, listening to the sound is a experience I can’t describe. In any case, it’s not a mistake holding some physical silver. COMEX/LBMA price shenanigans, so they have lost credibility. Shanghai SGE is for real as one can cart out silver bars. It does take sober thinking to see silver (and gold) hold their value against falling currencies. Did I just read about another emergency injection by the FED? Also, one can price cattle, housing and even indices in PMs. Gives a different picture of valuations. One can use PMs to save up to buy a farm tractor or any other investment. Works more than fine.

Thanks for your comprehensive write-up on silver.

Excellent piece. Most probably an excellent investment too, for the patient.